Did you know that gold is extremely ductile? A single ounce of gold (31.10 grams) can be stretched into a gold thread 8 kilometers long? Welcome to our Quarterly Report on Gold. The report provides a deep insight into the performance of gold over the 3rd quarter of 2022.

Global Jewellery Demand Performance

Key Highlights

- Global jewellery consumption grew by 10% (year-on-year) to 523 tonnes in Q3, a 14% jump from Q2.

- Jewellery demand manages to surpass its 5-year average of 501 tonnes.

- Year-to-date demand reached 1,454 tonnes, a 2% improvement compared to 2021.

- Note: The report highlights the performances of China and India because they are the two biggest jewellery consumers.

How did China & India perform in Quarter 3 of 2022?

China

China experienced massive disruptions in Q2 due to the implementation of the "Zero-Covid" policy. The policy prevented investors and retailers alike from conducting business. However, in Q3, gold jewellery demand experienced a 58% (quarter-on-quarter) growth due to changes in investor sentiment and a decrease in local gold prices.

How has Chinese sentiment changed?

Persistent lockdowns, sluggish economic growth and a weak local currency, have encouraged jewellery consumption. 24Karat (99.9% pure gold) products are highly demanded compared to their lower purity counterpart (18K, 75% pure gold). Higher-purity gold products promote value preservation through lower yields and transparent labour charges.

Retailers actively promote heavier gold products to boost profits and recover from a weak Q2. Chinese investors hunted for heritage gold products such as antique gold bangles with higher gold purity. Evidently, the heritage product market has surpassed 18K jewellery in China.

What is the outlook for China in Quarter 4?

(WGC) World Gold Council analysts believe that Q4 performance for gold jewellery in China has more upside than downside potential. Seasonality and the government's efforts to boost jewellery consumption will aid economic activity in the sector. However, China's Covid policies may remain a barrier to generating growth.

India

India's performance in Q3 was impressive as it overturned the negative global expectations for jewellery demand. Urban investors drove jewellery demand as India's economic activity began normalising. Credit expansion has also added a positive outlook to jewellery demand. In several recently published articles, India's bank credit growth grew by 17%, touching a 9-year high by the end of Q3.

What is the outlook for India in Quarter 4?

WGC analysts have projected that India's outlook for the year is positive due to upcoming festivals and marriages. Despite its respectable performance, demand figures are not to be on a record-breaking path compared to Q4 2021 as higher inflation cripples rural areas.

Bar, Coin & Exchange Traded Funds (ETFs) Investment

Key Highlights

- Bar & Coin investment in Q3 grew by 36% to 351 tonnes but still remains unable to combat the 227-tonne outflow of ETFs.

- Interest rate hikes and a stronger $US dollar to combat rising inflation is a barrier to gold investment performance.

What is the outlook for Bar, Coin & ETFs?

In Q3, drivers for gold investment are high inflation and the resultant impact on interest rates. Bar and coin investors focused on hedging against inflation. In contrast, ETF investors reduced their holdings as opportunity costs rose from interest rate hikes and the surging US dollar.

How did ETFs perform in Quarter 3?

Global ETFs positions experienced negative outflows of 227 tonnes (US $12 billion) for Q3 reducing the total holdings to 3,548 tonnes. Five straight months in Q3 have almost successfully reversed inflows of 316 tonnes generated between January - April 2022.

How did European ETF perform?

Europe ETFs saw inflows of 41 tonnes earlier in the year due to uncertainty surrounding the Russia-Ukraine war. However, Q3 performance saw a net outflow of 78 tonnes because of interest rate hikes imposed by central banks such as the ECB, SNB and BOE.

How did North America ETF perform?

In North America, ETFs generated the most substantial outflow of 149 tonnes to global gold ETFs. The Federal Reserve's hawkish approach to monetary policy altered investor sentiment. Investors sought to adjust their investment portfolios for higher interest rates.

How did Asia ETFs perform?

ETF performance in Asia saw a marginal inflow of 1 tonne during Q3. China influenced ETF performance in Asia as Chinese investors increased their gold holdings due to lower local prices. In India, ETFs were a net outflow of less than 1 tonne as higher returns on local equities and bonds attracted investors.

How did Bars and Coins perform in China?

In Q3, the performance of gold bars and coins grew by 8% year-on-year to 70 tonnes as a result of the following:

- The easing of lockdowns prompted the release of pent-up demand for gold products.

- In July, local gold prices experienced a pullback, initiating investors to bargain hunt for higher purity gold products.

- Chinese banks have advocated the benefits of physical gold products, attracting many investors.

WGC analysts suggest that gold as a "safe haven" and Chinese commercial banks' promotion of physical gold products should support overall demand.

How did India perform in Quarter 3 for Gold Bars and Coins?

India's performance saw an improvement of 6% year-on-year as retail investors reacted to the lower local gold prices and weaker equity markets. Q3 demand was 14% higher than the five-year quarterly average, the highest since Q1 to Q3 2015. However, a recent increase in customs duty on gold saw imports interrupted. The result saw increased smuggling activities on upwards of 29 - 30 tonnes of gold. Traders were exploiting a loophole that allowed them to import gold as a platinum alloy, paying a lower customs duty.

The festive period of Navratri, Diwali and wedding seasons saw improvements in coin demand. Discussions with Indian traders indicate that the remaining months of 2022 should match the performance of 2021 Q4, the highest quarterly investment for nine years.

How did other countries perform?

Middle East & Turkey

Gold bars and coins' performance in the Middle East grew by 64% year-on-year (26 tonnes), the highest quarterly retail investment for four years. Influencers such as rising inflation and opportunities to purchase gold price dips drove investors. Retail investment in Turkey is also substantial, with recorded increases of fivefold. The 47-tonne record is the second-highest quarterly report seen from Turkey. Exceptional inflation levels and stable prices of the Lira saw a surge in demand.

Western Market Performance

In the West, inflation, weakened economic growth and persistent geopolitical tensions continue to fuel demand for gold bars and coins. US demand remains positive at 3% year-on-year as consumers express pessimism towards the US economy and rising inflation.

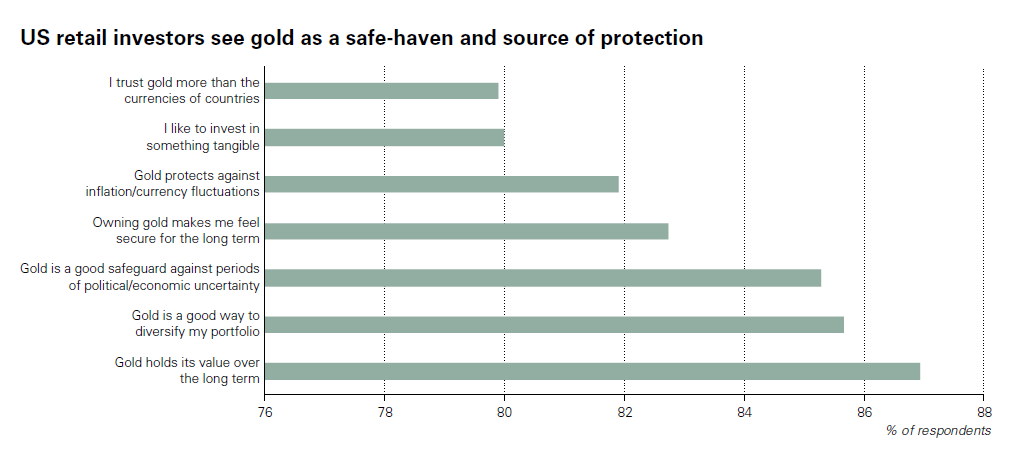

A recent study conducted by the WGC indicates that 82% of consumers believe that gold offers protection against inflation and currency fluctuations. 85% of respondents agree that gold is a safe haven against political and economic uncertainty. The remainder of prospects suggests that demand will remain healthy as more than 50% are "very likely" to buy gold coins or bars within the next 12 months.

Europe has also experienced a surge in gold investment by 28% year-on-year. Weak growth across the region, war, and central banks struggling to balance inflation continues to fuel gold investment.

ASEAN Market Performance

Investment demand remains robust across South East Asian (SEA) markets. The concern about inflation, currency depreciation and sustainability of medium-term economic growth remains troubling to investors.

Central Bank Performance

Key Highlights

- Q3 demand includes a significant estimate for unreported gold purchases.

- Turkey, Uzbekistan and Qatar were the largest buyers of gold in Q3.

- Year-to-date net purchases are at 673 tonnes, surpassing all annual totals dating back to 1967.

Global central banks accumulated 400 tonnes of gold in Q3 (115% quarter-on-quarter) increase. Generally, official institutions refrain from publicly reporting their gold holdings or may do so with some time lag. Metal Focus analysts suggest that purchases in Q3 may have started well earlier in the year.

Outlook for Central Banks on Gold

- Turkey remained the largest reported buyer of gold at 31 tonnes in Q3, increasing its reserves by 29% (489 tonnes).

- Uzbekistan added 26 tonnes in Q3, with a year-to-date purchase of 28 tonnes.

- Qatar bought 15 tonnes of gold in Q3; its total estimated reserves stand at 72 tonnes.

The demand trend for gold corroborates the WGC's findings from its 2022 Annual Central Bank Survey. A quarter of respondents in the survey indicated their intention to increase their gold reserves over the next 12 months.

What is the future outlook for Gold?

- The 2022 Financial Year remains weak for gold investment, but with certain upside potentials. These potentials are derived from global stagflation risks, fewer interest rate surprises and stretched negative sentiment. A stronger retail response and US dollar in a challenging environment may not be able to combat the lower over-the-counter (OTC) demand and flat ETF demand.

- Jewellery demand remained more robust than previously predicted. India and other SEA countries managed to support jewellery and fabrication needs, finishing 2022 with a better-than-expected position.

- Central bank demand will continue to be net purchasers of gold and outpace analysts' expectations, leading to further upside potentials.

Sources

Weekly Gold Investment Series Guide

Checkout our blog weekly or subscribe to our newsletter for the latest Gold Investment Guides

Click here to visit our Blog

Click here to Subscribe to our Newsletter

Disclaimer

The information provided on this website are adapted from the original authors and other contributors. These views and opinions do not necessarily represent those of ASTONM ENTERPRISE staff, and/or or any/all contributors to this site.